Table of contents

Bank API integration: overview, examples, and benefits

A bank’s business customers often prefer to work out of their own enterprise resource planning (ERP) solution to perform key financial activities.

As a result, these customers want their bank to seamlessly plug into their ERP systems and facilitate quick and accurate bidirectional syncs across a range of financial data.

We’ll break down why APIs are the best method for facilitating these integrations. We’ll also explore how banks can benefit from offering HRIS integrations.

But first, let’s align on the definition of an API integration for a bank.

What is an API integration for banks?

It’s any API-based integration that’s built between a bank and a 3rd-party application (typically either an HRIS solution or an ERP system).

Bank API integrations can apply to one of two scenarios:

- You work at a bank that offers integrations to business customers (i.e., customer-facing bank integrations)

- Your employer—which isn’t a bank—connects at least one of their applications to their bank (i.e., internal bank integrations)

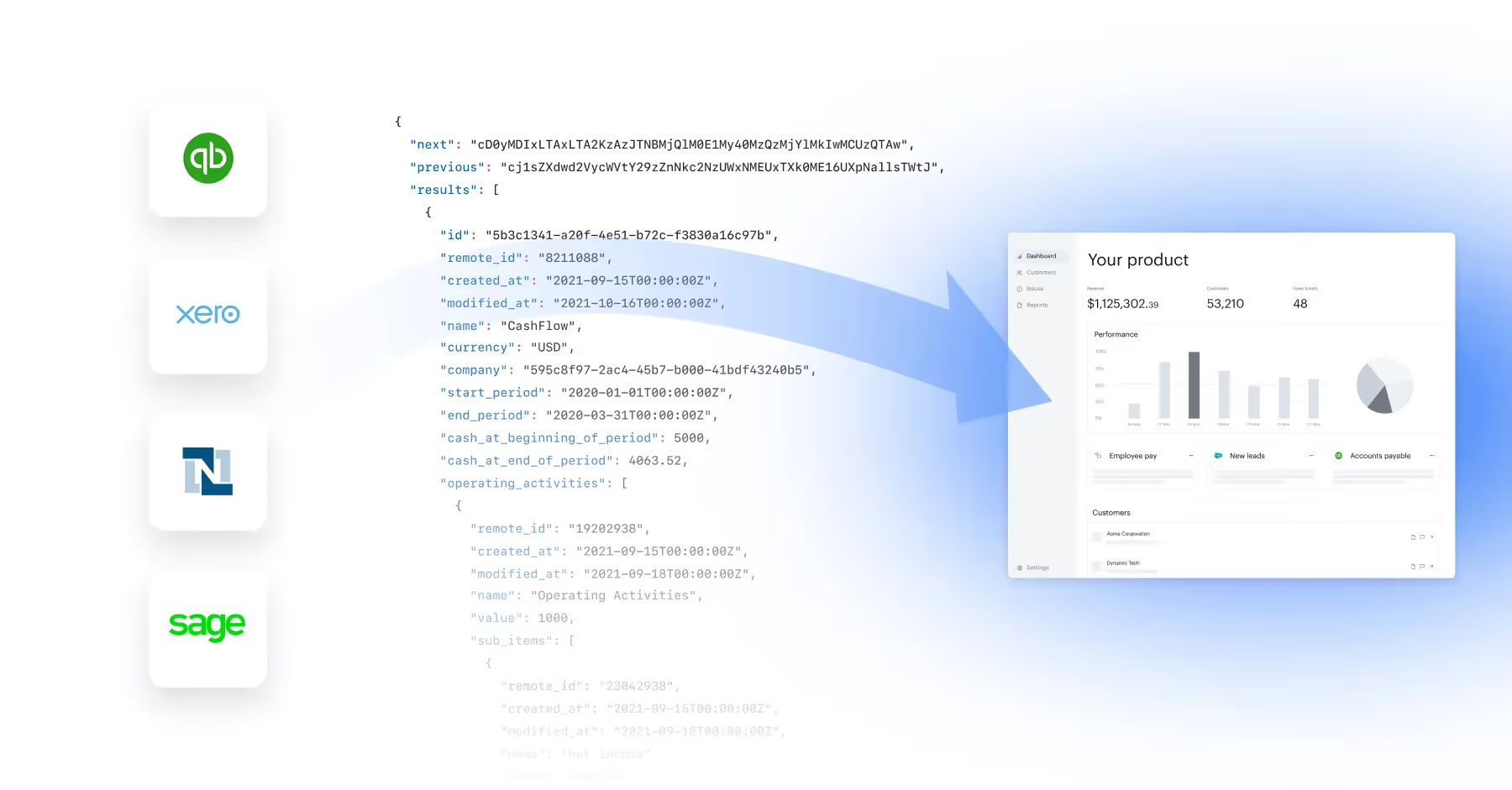

.webp)

Once a connection gets established, specific types of financial and employee data can sync between the 3rd-party application(s) and the bank on a predefined cadence (e.g., hourly).

It's worth noting that open banking is often mistaken for bank API integrations. Open banking is a system that allows external developers to access and build to a bank’s endpoints; the bank itself isn’t actively building integrations.

Related: What is a bank feed API?

Why banks need API integrations

Banks typically have a few options for integrating with ERP systems: scraping data at the UI level, exporting and importing files, leveraging API endpoints, and exposing API endpoints for customers to build into their systems.

Here’s why the last two options work best for supporting banks’ integration requirements:

- Security: APIs typically require specific authentication credentials to validate the consumer’s identity and scope of permissions. APIs also encrypt data in transit and use rate limits to prevent denial-of-service attacks. And while file-based integrations offer some level of security through SFTP, and scraped applications can require hardcoded credentials, both approaches lack the comprehensive security APIs provide

- Performance: APIs can share data in frequent intervals (e.g. every 10 minutes). They're also consistently reliable. For example, unlike screen scraping, a UI change in an application wouldn’t break the associated API-based integration. And unlike file-based integrations, the automated data flows APIs enable can prevent data integrity issues associated with manual intervention

- Accessibility: The vast majority of HRIS solutions and ERP systems offer comprehensive endpoints for the different types of data they create and store. This makes APIs well suited to support all, if not most, of the one-way or bidirectional syncs you want to build

{{this-blog-only-cta}}

Examples of API integrations for banks

While banks can leverage API integrations in a number of impactful ways, here are a few of the most popular use cases:

Note: The following examples focus on customer-facing use cases.

Run corporate card programs successfully

Any bank that offers corporate card solutions wants customers to adopt them quickly and with few issues.

With this in mind, a bank can integrate with customers’ HRIS solutions and build the following flow: Once customers add employees to their HRIS, the bank will automatically provision them access to a corporate card for certain types of transactions and spend limits (both depend on the rules the customer sets for employee roles, departments, locations, etc.)

Just as valuable, the bank can leverage the HRIS integration to implement a flow where once an employee is marked as terminated in the integrated HRIS, they automatically lose access to their corporate card.

Related: A guide to B2B API integration

Enable easy invoice reconciliation

A vendor can perform a seamless, error-free accounts receivable process by using a bank that’s integrated with their own ERP system.

Here’s how the process can work:

.avif)

1. The vendor would create an invoice through their bank and send it to their customer. The invoice data that gets created (e.g., invoice amount, date, currency, etc.) would sync with the vendor’s ERP system.

2. The customer makes the invoice payment through the bank, and the transaction data associated with the payment gets added to the vendor’s ERP system.

3. The vendor’s accounting team can go on to reconcile the payment within their ERP system.

Allow customers to pay and reconcile bills

Vendors can also help customers manage accounts payable activities with ease by using a bank that can integrate with customers’ ERP systems.

Here’s how:

1. A vendor invoices a customer, which, for the sake of this example, the customer goes on to accept.

2. The customer processes the invoice, which can involve getting it approved by internal stakeholders, categorizing the invoice, etc.

3. Once the invoice is processed successfully, the customer goes on to pay the vendor through the vendor’s bank.

4. The bank sends the payment data to the customer’s ERP system. This can include the payment date, amount, currency used, type of payment, etc.

5. The customer’s accounting team can go on to reconcile the bill within their ERP system.

Solutions for building bank API integrations

To implement any of the use cases above, banks can either rely on their own developers (“native integrations”), expose API endpoints so that customers can build the integrations, or use a 3rd-party solution (“3rd-party integrations”).

Native integrations

In-house, or native, integrations are defined as any that the bank’s own engineering team implements and manages.

Pros:

- Gives banks full control over their integrations’ health and performance

- Banks can task the engineers they know and trust to work on the integrations (as opposed to engineers they aren’t familiar with)

- Banks can build highly custom integrations to meet their customers’ specific needs

Cons:

- API integrations are extremely time and resource intensive to build and maintain. This forces banks to make difficult decisions on prioritizing their integrations and deciding between building and enhancing their core banking features and their integrations

- Banks may not have engineers with experience in building to APIs and/or managing the connections. As a result, onboarding them to these projects can take a while; alternatively, banks can recruit expensive engineers to take on this work

- Banks may have to form expensive partnerships with API providers just to access their sandbox accounts and API documentation

Related: The pros and cons of native integrations

Exposing API endpoints for customers

Often used by larger, legacy banks, this approach puts the onus of building and maintaining integrations on customers.

Pros:

- The banks’ developers don’t have to build and maintain the integrations

- Banks can provide 3rd-party integration services to customers—allowing customers to also avoid building and maintaining the integrations

Cons:

- Slow time to value, as customers can take months to build to their banks’ endpoints

- Leads to a poor customer experience, as customers’ engineers will likely get bogged down with maintaining the integrations over time

- If the bank offers a 3rd-party integration consultant or vendor, that’s another cost that the customer incurs

3rd-party integrations

3rd-party integrations are any that a bank outsources. This can include any part of an integration’s lifecycle, from testing an integration to maintaining it over time.

Pros:

- Using a unified API solution, banks can build to a single, aggregated API and access dozens of HRIS and accounting integrations out of the box

- Certain vendors have sandboxes available for testing, allowing your team to avoid expensive partnerships

- Specific vendors also have comprehensive and intuitive integration observability features, such as fully-searchable logs and automated issue detection functionality. These features can enable the bank’s customer-facing teams to diagnose, troubleshoot, and resolve integration issues themselves

Cons:

- Legacy 3rd-party vendors often lack the flexibility banks need to support their customers’ syncing requirements

- Legacy integration solutions may also force banks to build one integration at a time, which, depending on the banks’ integration needs, may not be scalable

- Many nascent 3rd-party solutions may not live up to their product promises and go out of business within a few years (if not sooner)

Final thoughts

The banks that can build the most robust, reliable, and in-demand API integrations will likely become market leaders for years to come. As a result, the question isn't whether your bank should build API integrations or which should be prioritized—it's how you go about building and maintaining them effectively at scale.

{{this-blog-only-cta}}

.png)